The Business Model of VCs vs. Venture Debt Funds

Note: This is the second in a series of 6 posts on venture debt.

As mentioned in a prelude recently, Venture Debt is often a commonly misunderstood source of capital for growing SaaS startups.

In order to fully understand why, let’s start with breaking down the business model of a VC (Equity) and Venture Debt fund.

VC (Equity) Fund

The Pareto principle applies to VC funds — 80% of returns come from 20% of startups.

Below is an illustrative VC business model taken from a TechCrunch article published last year.

Source: Money Talks, Gil Ben-Artzy

Limited Partners (or “LPs”) — the family offices, institutions, corporates, pension funds, endowments, sovereign wealth funds, and fund of funds that invest in funds — expect at least a 3x return on capital committed and invested over a typical 10-year VC fund life. This equates to a minimum internal rate of return (“IRR”) of 12% annually. (In reality, top quartile VC funds perform much better.)

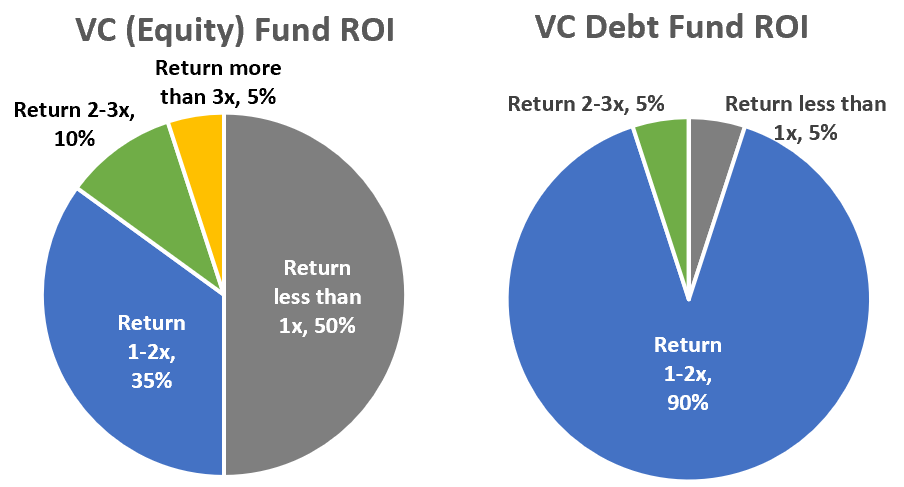

An overwhelming majority of early stage investments ‘fail’ (i.e. 50% of invested capital provide less than 1x return on capital and are effectively written-off). Most of the return for VC funds come from 20% (more or less) of invested capital. This implies that the minimum IRR for each investment — in other words, the annual growth in value of a business —is at least 60%.

For a scale up business (in Europe, this would be classified as a Series A/B investment), this means that 60% is often the minimum growth rate expected by VC funds — either by increasing top line revenue and/or expansion of enterprise value multiple.

Another reality of VC-backed businesses is that by default they fall into 3 buckets:

The Rockstars* that aspire to become a Unicorn — a VC fund will want to invest as much capital as possible in this rare breed,

The Dark Horses where a VC will invest energy, time, and provide access to their network in hopes they are Rockstars, or

The Walking Zombies that never quite figure out their product-market fit or commercial scalability.

Since most of the fund’s return comes from top performing businesses, the VC model is heavily reliant on identifying and building ownership stake in the Rockstars that will become real Unicorns and guiding the Dark Horses as far as possible in their journey.

Venture Debt Fund

Venture Debt funds, in comparison, are expected to deliver half the returns of a VC fund. A top performing venture debt fund can deliver 1.5x return over a 10-year period.

The main differences are:

The ‘failure rate’ is much lower for a Venture Debt fund — 5% or less of invested capital is written-off — due to the pre-screening of investment opportunities through VC funds and, sadly, sometimes the unwillingness of VCs to ‘let go’ of startups that have been funded and ‘drip fed’ resources for far too long.

A Venture Debt fund is a yield instrument. This means that fund income is generated through a steady and frequent stream of future cash expected (In contrast, VC funds provide multiples return through only two cash entry and exit points — when you initially invest in the business and when you sell the investment — with a long holding period in between). The Venture Debt fund returns borrowed capital and generates income through the (i) coupon or interest paid monthly, (ii) closing/transaction and maturity/end of loan fees, (iii) repayment schedule, and (iv) warrants. Warrants are the ‘sweetener’ that allows the debt fund to participate in the upside that a VC fund has by taking options in the business (typically priced at the most recent round’s valuation) later converted into shares on a cashless basis in an exit event. The first three really drive the IRR (i.e. yield) and the last variable impacts the fund return multiple. In most cases, the typical structure of a venture loan assumes initial capital borrowed is returned in the first 15–18 months of a 3-year loan and the remaining capital is then profit to the fund. (I will discuss market terms for European loans and how to best negotiate in a separate post.)

In addition, a Venture Debt fund re-invests capital committed at least once (i.e. ignoring management fees, a $100MM fund can recycle and invest over $200MM of capital to startups). This mechanism is usually quite limited for VC funds.

A European venture debt fund can generate ~10–13% IRR on debt alone and ~20% (and up to 30% or higher in certain cases) when including warrants from successful VC exits.

The hurdle rate for growth in business value is much lower as a result of this fund model – in most cases, 20% will suffice. Almost all of a Venture Debt fund’s capital is provided to the Dark Horses (given excess supply of venture funding available for the Rockstars).

Bottom Line

There are key differences between the business model of a VC and Venture Debt fund (summarized below).

If you are a Rockstar* SaaS scale up, then both debt and equity can be raised.

If you are a Dark Horse aspiring to be a Rockstar, then debt is likely the most viable funding option until you are a Rockstar.

Since there is a cost to servicing debt (with equity) as well as a signalling effect, there is a more appropriate time to raise Venture Debt for a cash burning, fast growth SaaS business.

(Full disclosure: I spent 6 years advising and providing debt to European and US businesses from technology startups to public companies. The first two years of my venture career were spent as part of the founding team for Columbia Lake Partners, the European venture debt fund backed by the partners of Bessemer Venture Partners.)