Planning for a New World Order in Software and SaaS

Planning for a New World Order in Software and SaaS

“Risk comes from not knowing what you are doing.” - Warren Buffett

For successful entrepreneurs, business scaling and wealth creation takes place over one (perhaps two) economic cycles. Whether you’re building a business or investing into one, timing and resources are equally important. It is always best to enter a market that is picking up momentum and rise with its natural wave of opportunity.

As we reflect on 2023 and plan for 2024, it is a good time to acknowledge the obvious: we are in a critical, turning point in history. One that started to take shape many years before COVID, with this next chapter likely to be studied and debated for many decades to come.

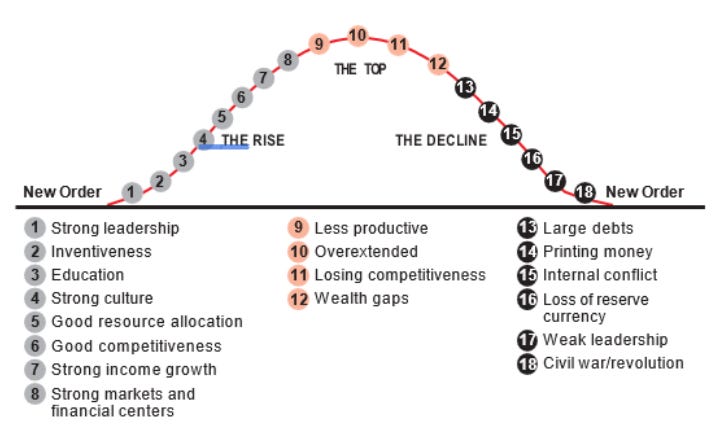

Systemic forces at play: a new world order is being defined

If you spend time reading on Reddit or watching Ray Dalio on YouTube (or consume more traditional sources of information and data), it is clear that over a decade of excess has had mixed-to-unfortunate economic, political and social consequences for humankind.

Germany has been in a recession this year and the UK’s economic growth also looks bleak, which means Europe as a whole is not growing or even shrinking. “Developing” countries have emerged as the new global leaders in production with economic activity exceeding those of mature nations since 2020.

On top of two horrific wars, we are facing an unprecedented number of climate threats that will impact ca. 90% of the world’s population, particularly those living in densely populated areas and low sea level regions.

Hoard cash: stabilize and strengthen the Balance Sheet, operate a predictable and lean P&L

With less money in circulation, higher costs for goods and services, and less income being generated, the effects of stagflation in simplest terms means: do more, with less. Most of our world’s working population has yet to experience this phenomenon. Those that have relive them as childhood memories or stories told by their parents.

It means that not only is money more scarce and valuable, but also institutions, businesses and individuals that manage money are less likely to part ways with it.

Many companies have cut costs with multiple rounds of layoffs, particularly evident in the technology sector, in an attempt to reach profitability and preserve cash.

A direct consequence is that new business sales have been slow. Businesses have prioritized internal organizational changes, as opposed to making new investment decisions such as buying solutions from external vendors. VC-backed private and public software companies are feeling the pain. In a recent LinkedIn post by Jeremey Donovan of Insight Partners (which has since surfaced new opinions by Sam Jacobs of Pavilion and Kyle Poyar of Openview), it takes 3.5-5x as much effort to reach a new outbound sales opportunity compared to 5 years ago.

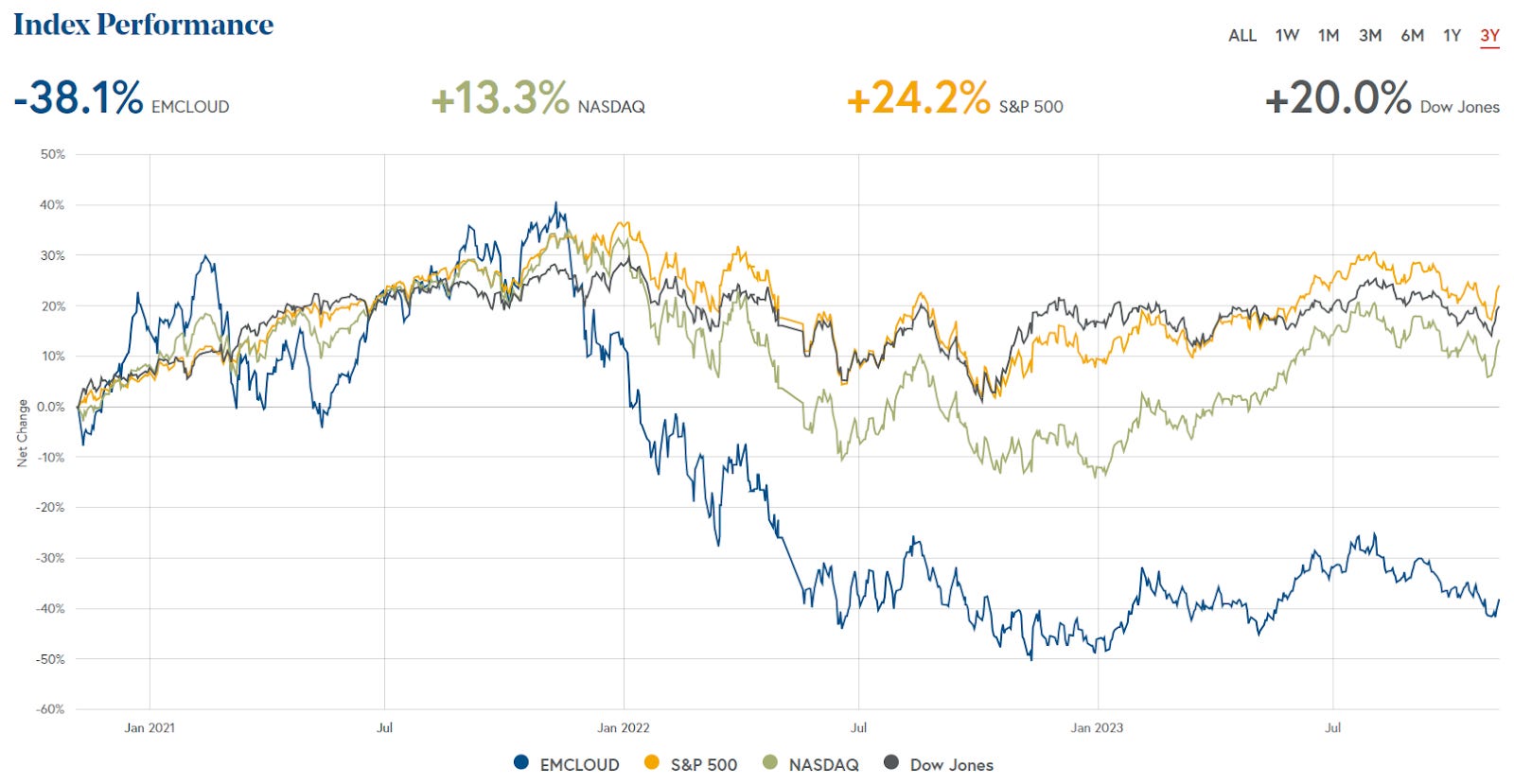

In spite of increased operational efficiencies (albeit at lower revenue growth), it seems software and SaaS businesses remain “out of favour” with institutional investors. Publicly listed cloud companies (represented by ticker EMCloud) continue to trade relatively low and have not recovered as much compared to other industry sectors (such as those represented in S&P 500 and Dow Jones indices) which are closer to early 2022 levels. The aggregate value of publicly listed cloud companies have declined by $1.7BN since its peak in November 2021, while valuations remain one-third of what they once were.

* Based on median quartile businesses in the BVP NASDAQ Emerging Cloud Index

Focusing purely on numbers, it is an evidently challenging business environment to navigate.

However, I am a firm believer that during times of chaos, there lies incredible opportunity if you can structure and capture it appropriately.

Optimize CapEx and minimize OpEx: sustainable businesses will survive, mission-critical technology will thrive

In order to cut through a noisy ‘echo chamber’, we must revisit and remind ourselves of (i) the first principles of scaling a business, and (ii) why SaaS became popular in the first place.

To create lasting business value, we need to:

Read, interpret, and influence change in the 3 financial statements that communicate business profitability and health:

P&L (or ‘Income Statement’), Cash Flow Statement, and Balance Sheet,Build commercial and operational excellence within an organization, and

Create value and balance incentives with existing shareholders, and secure more funding from the broader financial markets ecosystem.

In bull markets where money is cheap and plentiful, we are incentivized to grow revenue quickly in order to capture new market opportunities - this means focusing on high conversion rates, fast sales, big contracts, and short recruitment cycles. Buyers, investors, and operators alike tend to focus on making P&L decisions - so long as customers sign contracts, funding is available, and talent is plentiful.

When money becomes scarce, attention turns to cash which means optimizing working capital (NB: this should always be done!) and making the most of existing cash-on-hand, therefore cash management and Balance Sheet decisions.

Commercially and operationally this translates to an emphasis on quality of revenue from existing customers and empowering valuable talent to keep the business running like clockwork. It also requires quick, tactical decisions to adapt and capture the most opportunity in a frequently changing business environment. Close alignment of organizational design with cultural and financial incentives, as well as leveraging real-time data and business intelligence are critical to success.

Software-as-a-Service (“SaaS”) has experienced tremendous growth in the past two decades with Salesforce being one of its early business model pioneers. The key reasons are the relatively cheap and fast ability to build and distribute software, which was previously only accessible to companies that could afford its own infrastructure (often enterprise). This meant software became accessible to all types of buyers - a diverse set of businesses and consumers; and as a result, new SaaS solutions were born and grew quickly to tackle problems where legacy software vendors were slow to serve or regarded as too niche.

From a business perspective, what was traditionally a capital expenditure on the Balance Sheet (i.e. on-premise software) became an operating expense in the P&L (i.e. SaaS). By extension, this also meant that a buyer believed a cheaper SaaS solution could provide more immediate return-on-investment (“ROI”) compared to human capital, with possible medium-long term benefits that outweigh upfront investment into expensive software infrastructure.

Early SaaS solutions focused on collecting and connecting valuable data as well as reducing workload for specific business functions (Alex Kayyal of Lightspeed explains the utility and eras of SaaS in a simple framework). However, as software vendors transitioned into the cloud and became more modern through M&A and strategic partnerships & investments, they were able to also capture SaaS expertise and market share. Microsoft, Salesforce, Workday, Intuit, and Oracle are some examples of companies that have done this successfully.

Core thesis today

In our new world order of capital scarcity and resource sustainability, I believe that leading software businesses will demonstrate not only P&L efficiencies for their customers (via cost reduction and revenue increase), but they will also measurably optimize resources on the Balance Sheet.

Prediction #1

SaaS solutions will likely find more commercial success by serving businesses in traditional, asset-heavy industries which are undergoing significant digital and data transformation and/or companies that provide mission-critical infrastructure that can become more capital efficient using software.

The US Series A investments data from last 6 months provided by Peter Walker of Carta seem to provide signals that some early investors share this thesis.

Prediction #2

SaaS companies with low cost distribution models often found in integration-rich, PLG and community-centric, marketing-led organizations will thrive. While typically being more capital efficient and “sticky”, these businesses can combine a consumer-like user experience with data and business intelligence automation, thereby empowering employees to make effective decisions and take immediate actions that move a business forward faster.

Prediction #3

According to Statista, the SaaS market is expected to reach ca. $230BN next year, a growth of 7.5x over the past decade. Globally, there are over 10K private funds that invest in SaaS businesses today. I believe this buying and investment behaviour will continue to persist. However, I expect more consolidation among SaaS tools as software vendors with strong Balance Sheets and entrepreneurial teams capture innovation through integrations, partnerships, and M&A.

What does this mean for 2024 planning?

Detailed, data-led top-down strategy and bottoms-up capacity planning is critical to achieve accurate forecast, business growth and capture funding

Product and business roadmap decisions should prioritize the strategic finance needs of your customers

Maximize product and digital content distribution, and also optimize human interactions within specific channels for your target buyer

Carefully select which industry verticals, customer segments and geographies to pursue (and also avoid)

Be tactical in leveraging multiple Balance Sheets to grow (i.e. partnerships or M&A)

Preparing for 2024 and a new world order should be the #1 priority for every business over the next 4-6 weeks.

As a long-time advocate for SaaS, Pegafund is hosting an AMA webinar to discuss and debate 2024 planning and budgeting.

We welcome you to join us - please reach out if you would like an invite.

Very well researched and a thoughtful macro perspective. What companies did you have in mind when making prediction #2?