ROIT: Compounding cash, value, growth, and AI

ROIT: Compounding cash, value, growth, and AI

"Data [literacy] is the new oil" - Clive Humby

I spent this week in New York City catching up with friends, former colleagues, and funds. One evening, I attended a SaaS executive dinner and sat next to an operating partner of a growth stage software fund. He was intrigued to understand why I had left the VC/PE world to build a fractional CFO business at the start of COVID. In my prior post, I outlined the rational reasons for doing so. I shared during our conversation the personal motivations behind it.

I first started studying accounting and economics in 2003 purely due to curiosity and practicality. In the aftermath of a bad financial decision, I wanted to understand how to make smarter financial choices, and how to not lose and also earn money in the process.

When I joined the industry in 2007 just as the Global Financial Crisis was starting to unfold, I became enthralled by the breadth of work, ‘hungry’ and clever individuals the industry attracted, and the opportunity to experience and understand the world better. Graduating in 2009 and being fortunate enough to get a bulge bracket investment banking job in NYC meant I learned the humility that every working professional is at some point ultimately replaceable. Customers, businesses, and industries self-select retention and progression. For me, this meant continuously upskilling and building a strong network so I would always have security in the labour market, irrespective of business cycles.

My #1 priority has never been about maximizing capital. It has always been centered on deepening my understanding and therefore value in a competitive global talent pool by experiencing where money comes from, how it moves from A to B, how businesses make money, and how individuals are incentivized and influenced. This has translated into taking on new roles in order to learn by doing - taking a craftsmanship approach I observed from many GenX and Boomers, particularly those in ‘Old World’ industries.

With the incredible advancements in AI, I have no idea how strong my current professional moat will be. The rules of engagement set by decades of globalization, distributed production and mobile knowledge workers, and widespread digitalization are being reconstructed at its core as we speak. I believe those who know how to allocate money (aka ‘capital allocators’) as well as shift people, product, and services (aka ‘resource allocators’) will have distinct unfair advantage going forward. LLMs are trained by asking the right set and sequence of questions on a big and relevant data set, and those with sizeable & stable balance sheets and large high quality datasets are much more likely to win in the years and decades to come.

Why? Because money is made when markets are not efficient.

And markets are not efficient due to (i) data, information, and relationship asymmetry and

(ii) human decision-making (which blends emotions and logic).

What is most important for businesses, industries, and economies are that expectations to grow have not changed, albeit now with less resources and higher cost. Therefore focussing on ROIT is key.

ROIT stands for “Return On Invested Time”. It is a made-up acronym I started using to remind myself and the founders we work with that time is a finite and scarce resource. People can be hired, money can be raised, but opportunity cost is tangible and measurable. AI makes sure of that. Everything compounds with time - skills, network, money and data.

Data when turned into information followed by actions which form habits have the power to influence individuals and businesses to be nimble and execute better. In practise, this does not happen as quickly as investors would often like as it is difficult to capture exponential (or even step-linear) growth in a dynamically changing environment with multiple interdependent variables. There is often a meaningful lead time to embrace a data-centric culture; and my personal experience has been that scaleups who are successful take twice as much time and capital to reach their initial goals. The key reason being is individuals and businesses also have inertia - a physics principle used to describe the natural tendency of an object to resist a change in motion, staying at the same speed and direction until an external force is applied. In this case, I believe the combination of COVID, shifting geopolitics and AI are these big forces at play.

With the advancements in the semiconductor industry challenging key assumptions underpinning Moore’s Law, VCs and businesses are piling money into AI ignoring fundamental financial valuation.

Why? It is not clear yet how the economics for building and running a company will change due to AI; although it is very clear that the disruption is much bigger than Cloud has been for software and SaaS.

Take a look at Nvidia (NASDAQ: NVDA) which only a few months ago had ca. $3.3TN market capitalization, which is comparable to the entire UK economy - this seems absurd when comparing a 34,000 employee technology business to a country with a diverse working population of ca. 33 million people (or ca. 48% of total population). From another point of view, this single business was valued 5x the PE/VC industry of ca. $645BN which employs ca. 12 million people across 18,000 funds.

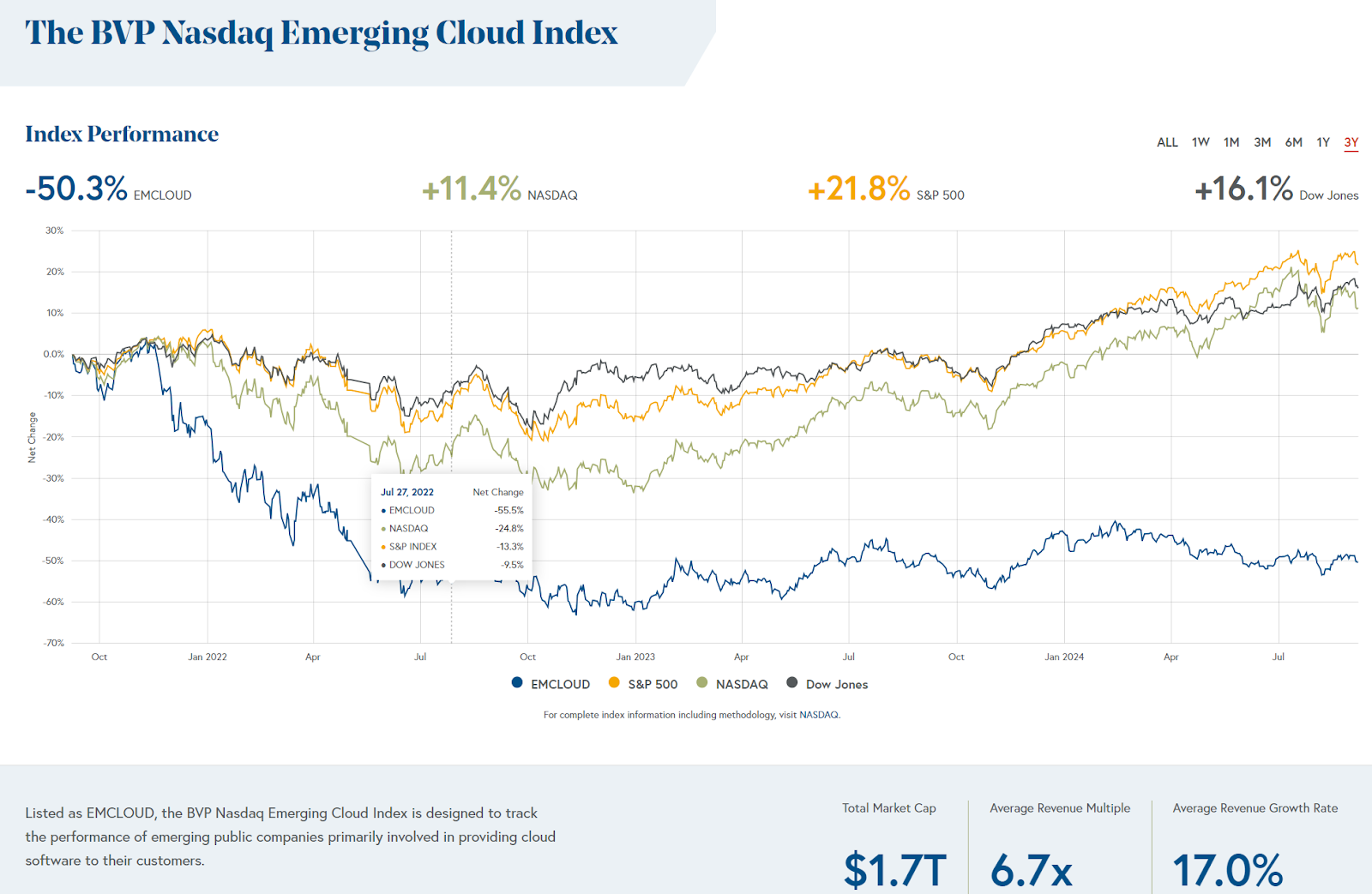

Perhaps this could be one of the reasons why public Cloud valuations remain depressed while other business models have recovered (see below). In fact, across the businesses we work with, I have also observed a meaningful shift in pricing structures for SaaS companies with a tendancy towards usage and performance-based pricing directly tied to their customers.

Preqin exited to BlackRock not so long ago at 10.6x this year’s estimated revenue for a business growing 20% in a market ca. $8BN with 12% forecasted annual growth. This is an important precedent set for valuing proprietary data businesses that generate recurring revenue at a premium compared to the average revenue multiples for public Cloud companies.

With undeployed private capital at an all-time high of ca. $2.6TN to be invested, businesses certainly cannot complain there is no money ready to be invested. However, new investment pace is still relatively slow simply because there continues to be a wide gap in expectations between founders and investors on valuations. Further, public market sentiment remains uneasy.

In late June, I was at a family office event in London where Aumni (JPMorgan) also presented. The team shared data which showed that more than 80% of VC-backed companies that raised during business cycle peak have not yet gone out to fundraise since the convertible rounds from existing investors in recent years. In addition, new investment deal volumes for VCs are less than half of its peak with 2 deals being completed per year per fund on average (compared to 4.6 during the peak in Q4’21 and Q1’22).

Based on all this, I suspect there will be a flurry of M&A activity next year, depending on economic data and geopolitics including the US election outcomes in Q4.

So as we round out Q3 and start planning for 2025, I urge you to think long and hard about the cash, value, growth, and data strategy for your business. Look closely and carefully at the numbers so that you can anticipate the right balance of all four components. I am certain that doing so will enable you and your business to be successful in the coming years and beyond.

We will be hosting another webinar on 2nd of October on the topic of “Fundraise and Exit: Data, AI, and Growth in 2025+”. Please leave a comment or reach out directly if you are interested in joining us.